On 7 October 2025, the FCA published a (the “Consultation”) on an industry-wide scheme to compensate motor finance customers who were treated unfairly between 2007 and 2024 (the “Motor Finance Consumer Redress Scheme”). The FCA has also set out steps and its expectations before finalisation of the Motor Finance Consumer Redress Scheme rules in the (“Dear CEO Letter”) that the FCA has sent to lenders and brokers alongside the publication of the Consultation.

Nikhil Rathi, chief executive of the FCA, expects that “there will be a wide range of views on the scheme, its scope, timeframe and how compensation is calculated. On such a complex issue, not everyone will get everything they would like. But we want to work together on the best possible scheme and draw a line under this issue quickly.”

The Consultation aims to balance several principles to deliver an easy-to-access and simple-to-deliver scheme, providing fair compensation promptly while ensuring the continued integrity of the motor finance market.

The Consultation departs from the usual three-month consultation period and will close on 18 November 2025 for comments on the overall design of the Motor Finance Consumer Redress Scheme and on 4 November 2025 for comments on the proposals to further extend how long firms have to provide a final response to certain motor finance complaints. If adopted, the Motor Finance Consumer Redress Scheme will be given effect through amendments to CONRED (the FCA’s Consumer Redress Schemes sourcebook).

Background

On 1 August 2025, the UK Supreme Court handed down its long-awaited judgment in Johnson v FirstRand Bank Ltd, Wrench v FirstRand Bank Ltd, and Hopcraft & Anor v Close Brothers Ltd, reported together as [2025] UKSC 33 (“Hopcraft Decision”). While fiduciary duty and bribery claims were dismissed, the Court upheld an “unfair relationship” under s.140A of the Consumer Credit Act 1974 (“CCA”), an outcome with clear implications where intermediary commission or contractual ties were not properly disclosed. For further information in relation to the judgement, please refer to our article here.

The FCA had signalled since March 2025 that it would consult swiftly to give certainty to firms, investors, and customers, and is now proposing to use its power to set up the Motor Finance Consumer Redress Scheme.

Firms and Vehicles in Scope

- Who delivers the scheme? The FCA proposes that lenders will operate the Motor Finance Consumer Redress Scheme, with brokers required to co‑operate and provide information promptly, including remitting complaints received to the lender for determination under the Motor Finance Consumer Redress Scheme.

Where liabilities have been assigned or acquired, the assignee would also be responsible for obligations arising from the Motor Finance Consumer Redress Scheme.

- What agreements are covered? The scheme would apply to regulated credit agreements used to buy or hire‑purchase a motor vehicle. These are most likely to be personal contract purchase (PCP), hire purchase (HP), or conditional sale agreements. Consumer hire (leasing) agreements are excluded because s. 140A of the CCA does not apply to hire. A “motor vehicle” is defined as a “mechanically propelled vehicle intended or adapted for use on roads to which the public has access”. The FCA does not provide an exhaustive list, but caravans and jet skis are given as examples out of scope.

- How does the Consultation describe the Scope?

- “Subject matter” defines the conduct issues addressed by the Motor Finance Consumer Redress Scheme, a relationship would be considered unfair where there was inadequate disclosure in connection with a motor finance agreement of one or more of the following:

- a discretionary commission arrangement (“DCA”);

- high commission (where the commission is equal to or greater than 35% of the total charge for credit and 10% of the total loan amount of credit, the relevant values are as at the start of the agreement); or

- contractual ties that gave a lender exclusivity or a right of first refusal.

- “Subject matter” defines the conduct issues addressed by the Motor Finance Consumer Redress Scheme, a relationship would be considered unfair where there was inadequate disclosure in connection with a motor finance agreement of one or more of the following:

As DCAs are already defined in the FCA Handbook, the FCA is only seeking views on the proposed definitions of high commission payments and contractual ties.

The 35%/10% threshold is the point at which the FCA’s analysis best indicates that borrowing costs may have been more strongly affected by the commission, such that its size would likely to have been a major consideration in the consumer’s mind had they been aware of it when they took out the loan.

The Consultation makes it clear that these thresholds are solely for the purpose of the design of the Motor Finance Consumer Redress Scheme and should not be read across to any other retail financial services market.

- A “scheme case” is an agreement the lender assesses under the Motor Finance Consumer Redress Scheme rules. To be a Motor Finance Consumer Redress Scheme case, there must be a relevant motor finance credit agreement and a commission payable by the lender to the broker; cases already finally resolved via court, the Financial Ombudsman Service (“FOS”), or accepted settlement are excluded.

Time Limitation

The Motor Finance Consumer Redress Scheme would cover regulated motor finance agreements taken out between 6 April 2007 and 1 November 2024 where commission was payable by the lender to the broker. The FCA is proposing that lenders will deliver the scheme, rather than brokers.

The FCA states that the start date aligns with the date on which s.140A of the CCA took effect. The end date is based on when the FCA expected firms to move to more transparent practices following the UK Court of Appeal judgment on 24 October 2024 that was subsequently appealed to the UK Supreme Court.

The Consultation sets out that consumers who have already been compensated for complaints covered by the Motor Finance Consumer Redress Scheme would be excluded. Consumers who have a live complaint with the FOS would have their case resolved by the FOS and not through the Motor Finance Consumer Redress Scheme.

Key Elements of the Motor Finance Consumer Redress Scheme

a. Consumer Consent Model (Opt-in/Opt-out): Customers who already complained to a firm (but not to FOS) are in scope by default unless they opt out, firms must contact these customers within three months of the start of the Motor Finance Consumer Redress Scheme.

All other customers must opt in, meaning firms must contact them within six months of the start of the Motor Finance Consumer Redress Scheme.

Customers who have not been contacted can approach their lender to review their case within one year of the Motor Finance Consumer Redress Scheme start date.

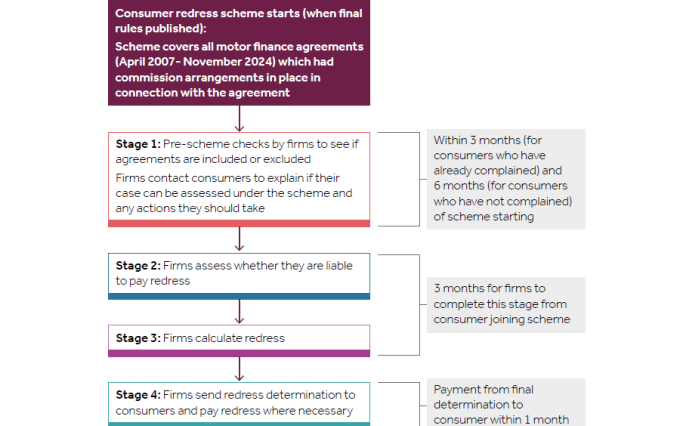

b. Four Stage Process and Timing: The Consultation sets out in four stages the proposed Motor Finance Consumer Redress Scheme and the steps lenders, brokers, and consumers will need to take. Please see the below flow chart that provides an overview of the proposed Motor Finance Consumer Redress Scheme stages and timings.

Source: .

c. Redress Calculation: Recognising the Hopcraft Decision, the FCA proposes that consumers whose cases align closely with the Hopcraft Decision should get the commission repayment remedy.

For most other cases, redress would be calculated using a hybrid approach that averages two methods, the commission repayment remedy and an APR adjustment remedy (which applies a reduced APR to reflect estimated financial loss). This approach aims to balance evidence of consumer loss with the broader range of remedies courts might award, given the uncertainty in cases that differ from the Hopcraft Decision.

In the very limited circumstances where the APR adjustment remedy would produce greater redress than the commission repayment remedy (if relevant) or hybrid remedy (if not), the FCA proposes consumers should get the APR adjustment remedy.

d. Possibility for Rebuttal: The Consultation proposes enabling lenders to rebut the presumption of unfairness in some limited circumstances. For example, lenders would be entitled to determine there was no unfair relationship under the Motor Finance Consumer Redress Scheme if:

- there is evidence of adequate disclosure of the relevant arrangement in question; or

- in cases only featuring a DCA, the lender can provide evidence that the broker selected the lowest interest rate at which they would not have made any additional commission; or

- disclosure of the relevant arrangement in question was inadequate, but the lender can provide evidence that the consumer was sufficiently sophisticated to have nonetheless been aware of the relevant feature(s).

Consumers may still refer such cases to the FOS, but only to check whether the Motor Finance Consumer Redress Scheme rules were followed or pursue a claim in court.

Extension for Handling Motor Finance Complaints

In anticipation of the Hopcraft Decision, the FCA has issued rules to extend the time firms have to respond and issue final responses in relation to motor finance complaints.

Under current rules, firms must start sending final responses to motor finance commission complaints, including those involving DCAs and tied arrangements, from 5 December 2025. However, this would require some firms to issue responses before the FCA concludes the Consultation and confirms whether the proposed redress scheme will proceed.

To avoid inconsistent outcomes and ensure complaints are resolved in an orderly and efficient way, the FCA proposes to extend the deadline for providing final responses to these complaints. This extension would give firms time to align their approach with the final scheme rules and avoid unnecessary duplication or consumer confusion.

It is important to note that the FCA proposes to exclude complaints about leasing agreements from the further extension.

Practical Points for Firms in Scope

The Consultation includes very detailed and prescriptive guidance on how the Motor Finance Consumer Redress Scheme should be implemented by firms. These include monthly data reporting to the FCA to demonstrate progress and compliance, the mandatory use of FCA-prescribed template letters for consumer communications, and a duty to notify the FCA promptly if financial or operational resources are expected to be inadequate. These requirements underline the FCA’s expectation that firms act early, maintain transparency, and ensure robust governance throughout the scheme.

The Dear CEO Letter therefore provides some additional practical guidance on what firms should focus on while the Consultation is ongoing.

The FCA’s Dear CEO Letter makes clear that firms should act now: resolve existing complaints fairly and get ready to deliver the scheme at pace if it proceeds. The FCA states that it will be pragmatic where firms are preparing seriously, but will intervene if they do not.

- Keep moving on complaints (with two timelines to manage)

- Leasing complaints: As mentioned above, the FCA is not proposing a further extension. Firms should plan to resume the standard 8‑week response timelines from 5 December 2025 and give any feedback on this point by 4 November 2025.

- Other motor finance commission complaints (non‑leasing): the FCA proposes to extend the deadline to send final responses to 31 July 2026. This is a pause on the final response clock, not a pause on investigation — firms should keep gathering evidence and continue to progress issues that fall outside any scheme (e.g., affordability/forbearance) under normal DISP rules.

b. Build “impacted customer” picture

Lenders should start working to identify and be ready to contact affected customers quickly once the Motor Finance Consumer Redress Scheme has been finalised.

c. Close data gaps with brokers

Lenders should assess what records are needed to test scope and liability. Brokers should prepare by cataloguing lenders used, commission/disclosure records and likely volumes, and by resourcing for lender requests. The FCA expects collaboration to be prompt and constructive.

d. Get case‑handling “fit for scale”

Lenders should review systems and controls to ensure redress can be calculated accurately and consistently at volume. The FCA encourages the use of technology, including AI, where it improves speed and consistency.

e. Resource prudently and avoid steps that hinder redress

Lenders should maintain adequate financial and non‑financial resources, provision or disclose potential liabilities appropriately, and avoid actions (e.g., asset movements, structural changes) that could delay redress. Brokers must also ensure, as a minimum, that they can meet debts as they fall due. Insolvency practitioners appointed over firms should continue to meet regulatory obligations.

f. Put clear senior ownership and robust oversight in place

The FCA expects that Senior Managers at lenders and brokers take responsibility for Motor Finance Consumer Redress Scheme readiness, with appropriate second‑ and third‑line oversight from the outset.

g. Stay open and cooperative with the FCA

The FCA expects that lenders and brokers engage proactively under Principle 11 and make SUP 15 notifications where anything could materially affect their ability to meet obligations (including resource concerns or contemplated transactions).

What Comes Next

The FCA will confirm by 4 December 2025 whether complaint handling deadlines will be extended. If the Motor Finance Consumer Redress Scheme goes ahead, the FCA expects to publish its policy statement and final rules in early 2026, with the Motor Finance Consumer Redress Scheme launching at the same time. On this basis, consumers would begin receiving compensation later in 2026.

What Firms Should Do Now

Lenders and brokers still have a window to influence the design of the eventual Motor Finance Consumer Redress Scheme. We strongly recommend that firms potentially impacted review the Consultation and submit comments on aspects of it that are of concern, e.g. the design, scope, calculation methodologies, opt-in/opt-out proposals. Firms should also engage now with trade bodies, industry groups and their legal advisors so their views are represented as impactfully as possible.

For further information, please contact ukreg@proskauer.com.

.